Crazy Eddie Crime Spree

The Crazy Eddie crime spree evolved in three phases:

(1) 1969-1979: Skimming and under-reporting income (tax fraud) prior to the big plan to go public

(2) 1980-1984: Gradually reducing skimming to increase profit growth in preparation for the initial public offering, i.e., committing securities fraud by “going legit”

(3) 1984-1987: As a public company, overstating income to help insiders dump stock at inflated prices using a variety of fraudulent tricks

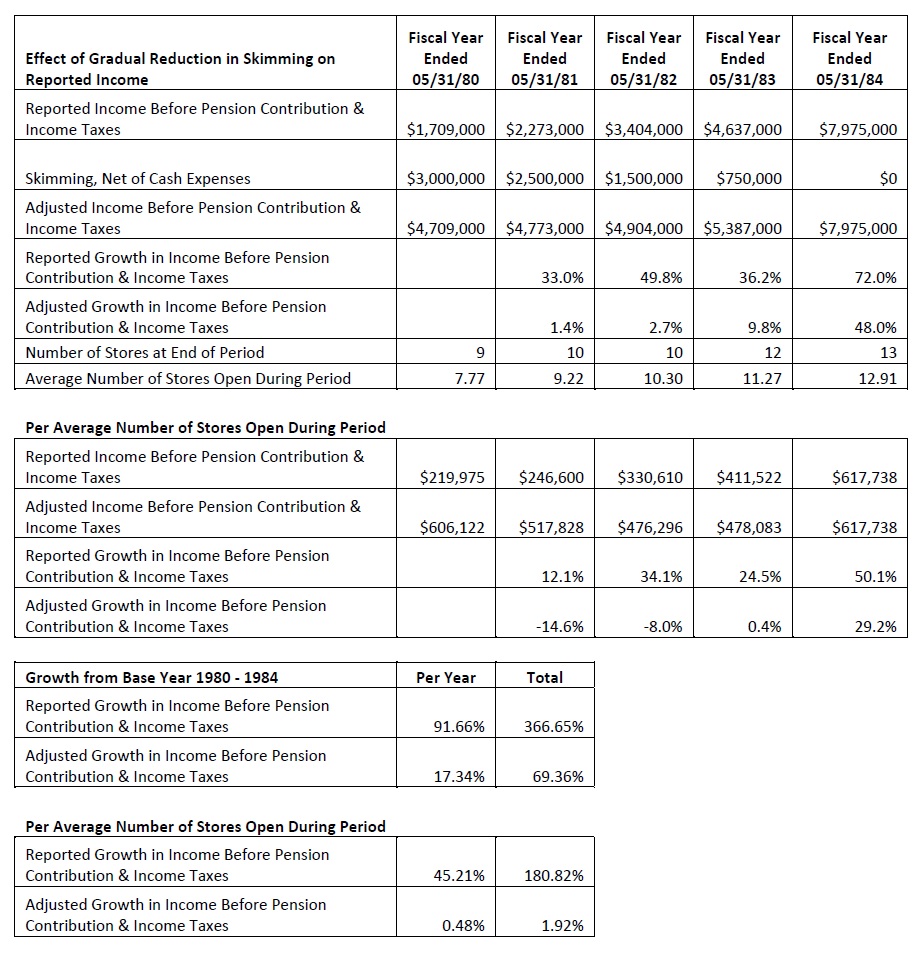

Gradual Reduction of Skimming in Preparation for Initial Public Offering (Fiscal Year 1980 to 1984)

The gradual reduction in skimming inflated reported pro forma earnings growth and store unit productivity growth in the fiscal years prior to Crazy Eddie’s initial public offering in September 1984.

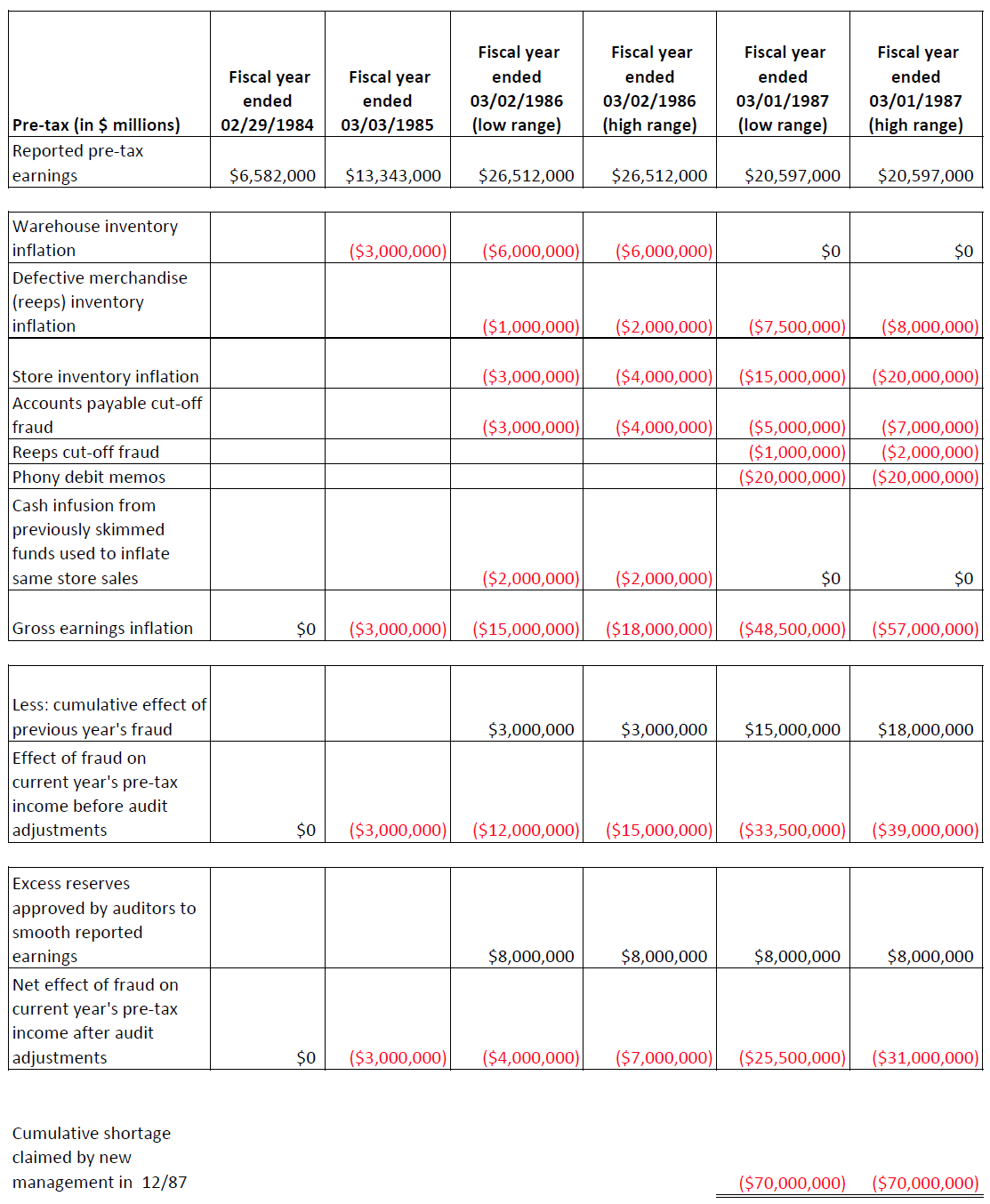

Inflation of Reported Income After Initial Public Offering (Fiscal Year 1984 to 1987)

After the initial public offering, Crazy Eddie overstated reported income to help insiders sell stock at inflated prices.

Notes:

The management team who gained control of Crazy Eddie claimed that its cumulative earnings inflation was approximately $70 million, while my calculations show that cumulative earnings inflation was $57 million. The differences in amount, though relatively small, can be primarily explained by alternative methodologies used new management and me to compute the scope of Crazy Eddie’s fraud. In addition, my computations extend only to the fiscal year ended 3/1/87, whereas new management’s computations extend to the period ended 11/30/87.

See Appendix B – Crazy Eddie Red Flags

Written by:

Sam Antar

© Copyright by Sam Antar. All rights reserved.