Why Society is Vulnerable to Fraud

White-collar crime is more brutal than violent crime. The actions of one or a handful of corrupt public officials and businesspeople can affect the livelihoods of thousands, even millions of people. Fraudsters use a combination of persuasion and deceit to execute their crimes. Unfortunately, most people are unaware of how easy it is for fraudsters to prey on their behavioral and cognitive vulnerabilities. Furthermore, the number of federal prosecutions for white-collar crime has steadily declined over the last 35 years. The government devotes far more resources to battling street crime than white-collar crime. The current framework involving compliance, audits, and law enforcement does little to protect investors from fraud.

Every person can commit a white-collar crime. At the 22nd Annual Conference of the Association of Certified Fraud Examiners Conference in San Diego California in 2011, Joan Pastor, PhD, Clinical Psychologist and Fraud Expert said, “We are all capable of committing fraud. Every single person in this room is capable of committing crimes.” For all of us, ethics is a matter of convenience depending on the situation and pressures involved. White-collar crime is an inevitable byproduct of the human condition. Seriously, can anyone truthfully claim that they live without sin and temptation?

At best, people can prevent themselves from being victims of fraud. However, there is little that our society can do to stop fraudsters from victimizing other naive and vulnerable people. If you are smart enough to avoid becoming victimized by a fraudster, they will simply find someone else with an exploitable weakness. Everybody has an exploitable weakness. The fraudster’s job is to find the people who have an exploitable weakness that he/she can take advantage of.

The Three Elements of Fraud

Fraud involves three elements: Perpetrators, enablers, and victims. All too often, people focus on the acts of the perpetrators and the exploitation of the victims. However, they ignore the crucial role of enablers in the execution of a fraud. Enablers can be the media, auditors, investment bankers, sell-side research, and others. They help the perpetrators of fraud gain implied credibility which helps fraudsters win the trust of their potential victims. Often, fraudsters use enablers as proxies to sell their message to potential victims or to quash adverse publicity. In matters of controversy, it is more credible for fraudsters to use their enablers as proxies to defend them rather than fraudsters trying to defend themselves.

Exploitable Weaknesses

White-Collar criminals use a combination of persuasion and deceit to achieve their objectives. Fraudsters prey on the psychological and cognitive vulnerabilities of their victims using the following techniques:

Fraudsters consider your humanity, needs, desires, ethics, morality, and good nature as weaknesses that they can exploit in the commission of their crimes.

Fraudsters measure their effectiveness by the comfort level of their victims. They use a combination of charm and deceit to achieve their objectives. It is far easier to get a potential victim to believe your lies if they like you.

Fraudsters fabricate false integrity to gain the trust of their victims. Stature, generosity, and virtuous deeds gain the respect of their potential victims and make it less likely that victims will question their behavior.

White-collar criminals will always have the initiative to commit their crimes. Your ethics, morality, and good nature limit your behavior, but fraudsters have no such constraints on their behavior. The ethical foundation of our society is based on trust and the legal basis of our society is based on the presumption of innocence. The inclination to trust and the presumption of innocence gives the fraudster the initial benefit of any doubt while they are free to plan and execute their crimes. Therefore, trusting, and decent law-abiding human beings are easier prey for fraudsters.

It is common knowledge that effective internal controls, oversight, and checks-and-balances reduce the opportunity for fraud. However, people tend to ignore the fact that their trust, ethics, and good nature limit their behavior and create a fertile opportunity for white-collar criminals to seize the initiative and execute their crimes. The behavior of fraudsters is not limited by ethical standards.

Distraction

When it comes to fraud, distraction is more effective than a lie. Distractions cause people to devote less attention to the fraudster’s actions and more attention to areas unrelated to their crimes. Distraction is less risky than lying and more importantly, it reduces the need to lie.

Crime and Punishment

Most people mistakenly believe that strong punishment such as long prison sentences is a major deterrent to white-collar crime. Recently, many white-collar criminals have received very stiff prison sentences, which I wholeheartedly support. At best, it holds those guilty of white-collar crime accountable and responsible for their actions. However, strong punishment does little to prevent white-collar crime. Often, we watch prosecutors pound the podium in front of the cameras and claim that their latest successful case sends a strong message to fraudsters to stop committing crime. However, white-collar criminals do not listen to the rhetoric of prosecutors. No white-collar criminal discovers ethical behavior and stops committing crime because another criminal ends up in prison. While white-collar criminals take precautions against failure, they do not expect to end up in prison.

Do not Trust. Just Verify

Trust is a hazard that will destroy your future livelihood. While you initially give a fraudster the benefit of the doubt, they will attempt to solidify their trustworthiness before you follow up to verify their claims. The fraudster hopes that you trust them enough to never verify their claims. However, if you later seek to verify their claims, your skepticism may be diminished by your increased comfort level with them. In other words, you will accept the fraudster’s deceptive answers as factual, even if you have some doubts.

A common mistake made by victims of fraud is called “unexamined acceptance.” Claims received from any source should not be taken for granted as being truthful and accurate without any critical analysis, investigation, and verification. Therefore, learn to exercise professional paranoia. Do not trust. Just verify.

Apologies

Apologies are irrelevant. While contrition and forgiveness are admirable traits, apologies do not change the past or undo the harm caused by fraudsters. Apologies tend to make the victims feel a small measure of comfort and make fraudsters, as a minimum, appear remorseful. However, apologies should not be relied on to predict future behavior. Judge people by their actions, not by their “well meaning” words or claimed “good” intentions.

Invisible White-Collar Criminals

According to the Association of Certified Fraud Examiners (ACFE) 2022 Report to the Nations on Occupational Fraud and Abuse, occupational frauds can be classified into three primary categories: asset misappropriations, corruption, and financial statement fraud. The report found that only 7% of fraud perpetrators had criminal records. As the economic impact of an economic crime goes higher, it is less likely that the perpetrators involved have any previous criminal records. Did Sam Bankman-Fried, Bernie Madoff, Ken Lay (Enron), Bernie Ebbers (Worldcom), or Dennis Kozlowski (Tyco) have criminal records? The answer is no. Therefore, it is difficult for law enforcement and professionals to profile the white-collar criminals among us.

Most Fraud is Discovered from Tips

The ACFE 2022 report found that, “tips were still the most common way occupational frauds were discovered in our study by a wide margin, as they have been in every one of our previous reports.” According to the report, “42% of cases in our study were uncovered by tips, which is nearly three times as many cases as the next most common detection method.” Only 16% of frauds in the study were uncovered by internal audits, 12% by management review, and 4% by external audits. The study found that 5% of the fraud cases were discovered by accident, more than the number uncovered by external audits (4%). A total of 47% of fraud cases were found by tips or accident. Unfortunately, our society must primarily rely on the actions of whistleblowers to inform us about most frauds.

Who are the Whistleblowers?

While the media often glamorizes whistleblowers, most of them are not motivated by altruism, but are motivated by revenge or personal gain. Every whistleblower has an agenda. To government investigators, it is known as the XXX principle (and I am not talking about pornography).

1. Ex-lovers: Divorced spouses, former girlfriends, and boyfriends.

2. Ex-business associates: Former suppliers and customers.

3. Ex-employees: Fired employees, laid off employees, and employees who quit working for the entity.

Whistleblowers can provide useful information. Most whistleblowers have an ax to grind and are looking to promote their personal agendas. They may have known about the crime during the execution of it but did not report it until later. A whistleblower’s credibility should be determined by the actionable verifiable information they provide, not what they say.

Do Audits Really Protect Investors?

Often, investors blindly rely on the integrity of audits to protect them against fraud. Unfortunately, audits give investors a false sense of security. Traditional financial statement audits of public and private companies are not designed to discover fraud. What accounting firms call an “audit” of financial reports is really a compliance review designed to find unintentional material errors in financial reports by examining a limited sample of transactions. In other words, traditional financial statement audits are like spell-checkers that are designed to catch the accounting equivalent of innocent typos without verifying the integrity of the underlying content.

Despite the built-in limitations of audits, the major accounting firms do a poor job conforming to professional standards and rules for carrying them out. According to a report issued by the Public Company Accounting Oversight Board, “Staff expects approximately 40% of the audits reviewed will have one or more deficiencies that will be included in Part I.A of the individual audit firm’s inspection report, up from 34% in 2021 and 29% in 2020:

Dwindling Law Enforcement Efforts to Battle White-Collar Crime

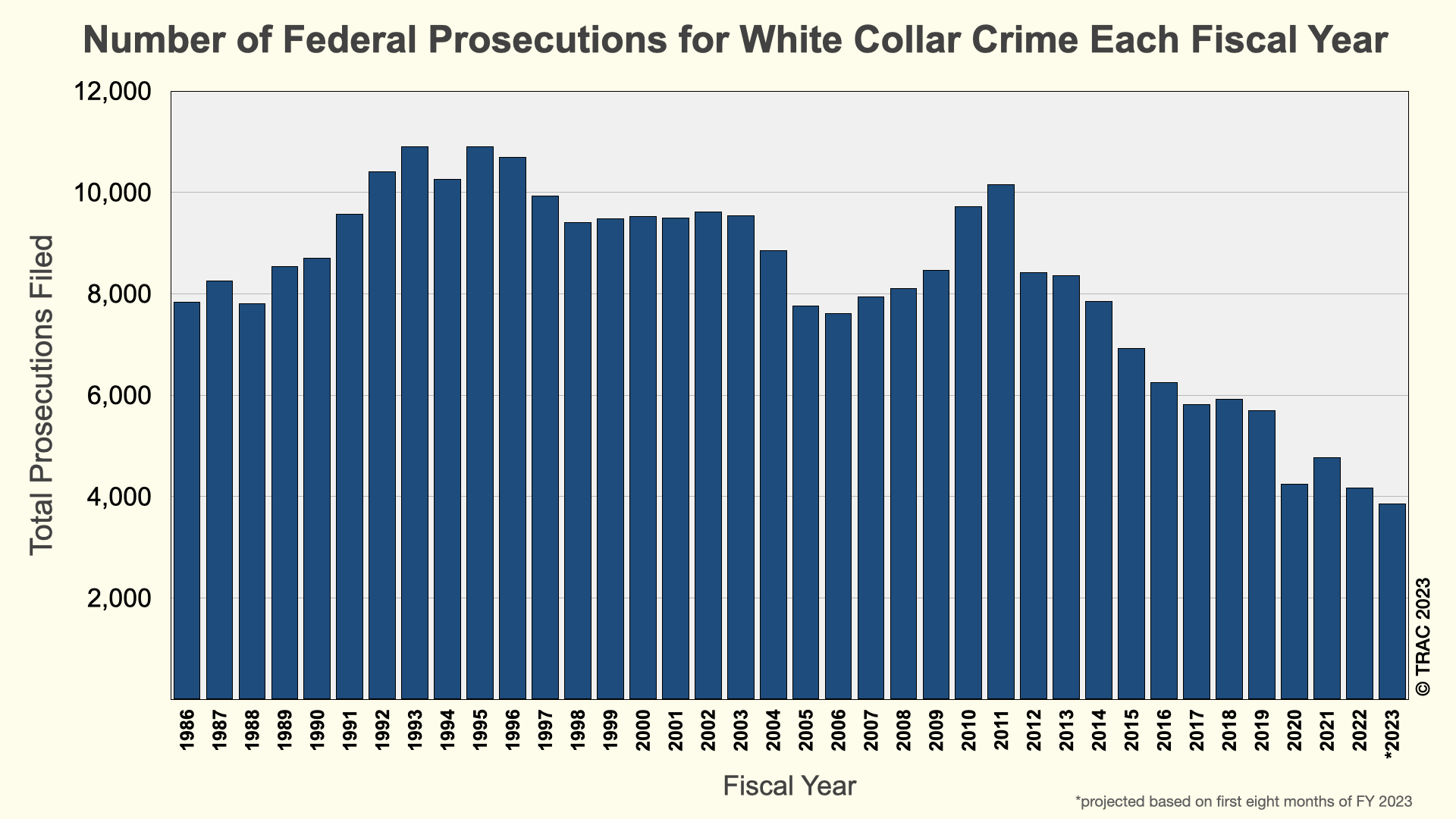

From 1986 to 2023, the number of federal prosecutions of white-collar crime has steadily declined, according to data obtained by Transactional Records Access Clearinghouse (TRAC) under the Freedom of Information Act from the Department of Justice. From 2014 to 2023, there were fewer federal prosecutions of white-collar crime than there was during my last two years of involvement in the Crazy Eddie fraud (1986 and 1987) while the gross national product is five times higher than 1986/87.

See the chart below:

As a nation, we devote far more resources to fighting blue-collar crime or street crime than we do battling white-collar crime. For example, the NYC Police Department employs approximately 34,000 police officers in uniform battling street crime. However, the FBI employs approximately 10,100 special agents, the IRS Criminal Investigative Division employs approximately 2,100 special agents, the SEC employs approximately 4,600 people, and the US Postal Inspectors Office employs approximately 1,250 criminal investigators. The NYC Police Department has more officers directly battling street crime than those four federal law enforcement agencies combined have been fighting nationwide white-collar crime.

Written by:

Sam E. Antar

Note: Originally published on 07/08/2014 and updated on 11/21/2023.

© Copyright by Sam E. Antar. All rights reserved.