Public filings show overlapping control, same-day reciprocal reporting, shared political operations, and nearly $79 million in charitable-to-advocacy funding flows — raising questions regulators should not ignore.

Thirteen days before Election Day, $950,000 moved from one Working Families committee to another. The same treasurer appeared on both sides of the transaction. The receiving committee altogether spent $1.8 million on “independent” expenditures supporting Zohran Mamdani for Mayor. This is where questions about Mamdani campaign coordination begin.

By law, independent expenditures must not be coordinated with candidates or campaigns. But when the same treasurer appears on both the giver and the spender — when organizations publicly describe themselves as “partners” while filing as independents — when $45,697.14 flows one direction and the exact same amount is recorded flowing back the same day — independence becomes a question worth asking.

This is the story of nearly $79 million in identified 501(c)(3)-to-501(c)(4) transfers that moved through a web of nonprofits into political committees that deployed over 147,000 door-knockers and spent millions supporting one candidate. It’s the story of shared treasurers, same-day reciprocal reporting, and organizations that called themselves “partners” in public while claiming independence on their filings.

And it ends with a woman who appears in the network’s tax filings as a senior officer getting appointed Deputy Mayor by the candidate who benefited from it all.

The public record contains enough overlap, money movement, shared infrastructure, and same-day reporting precision that regulators should have to examine whether this was truly independent — not why anyone is asking.

Substance Over Form

The filings describe separate entities: 501(c)(3) charities, 501(c)(4) advocacy groups, PACs, and independent expenditure committees.

But tax and election-law review should not stop at labels. It examines substance — how money moves, how decisions are made, and how organizations actually operate.

When funds flow from charities to advocacy groups to PACs to IE committees — while overlapping parts of the network show shared treasurers, vendors, addresses, field operations, funding relationships, and public “partnership” language — regulators should examine the whole chain, not merely each legal box in isolation.

The issue is whether overlapping parts of the network functioned as an integrated political operation while preserving formal claims of independence.

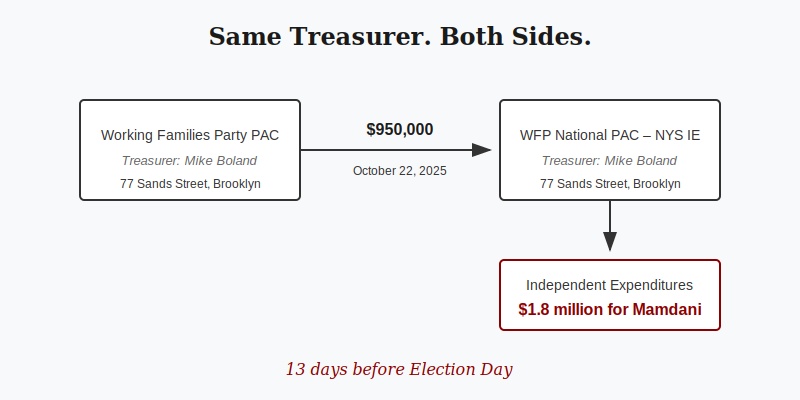

The $950,000 Transfer

Start with October 22, 2025.

Working Families Party PAC transferred $950,000 to WFP National PAC – NYS IE Committee. Thirteen days before voters went to the polls. (NYC Campaign Finance Board – Contribution Record)

Both committees list the same treasurer: Mike Boland. (FEC Committee Profile – Working Families Party PAC; NYC CFB – WFP National PAC NYS IE)

Both are managed by the same company: Community Labor Administrative Services Inc.

Both operate from the same address: 77 Sands Street, Brooklyn, NY 11201.

The IE Committee later reported $1,815,447 in independent expenditures — $737,278 supporting Mamdani, $978,370 opposing Andrew Cuomo. (NYC Campaign Finance Board IE Profile)

Here’s the problem: under New York Election Law § 14-107-a, PACs cannot contribute to IE committees if they share “common operational control.” The statute defines that as “the same individual or individuals exercise actual and strategic control over the day-to-day affairs of both.”

Mike Boland appears as treasurer on both sides of the reporting structure. The IE profile also identifies Joe Dinkin as authorized representative. That overlap does not prove common operational control, but it warrants examination.

The Second Circuit’s reasoning in Vermont Right to Life Committee v. Sorrell (2014) is relevant by analogy: the court found that entities claiming to be “independent” were “functionally indistinguishable” due to shared management and “fluidity of funds” — despite having separate bank accounts and organizational documents stating they were independent. Formal separation, the court held, does not end the factual inquiry.

Same treasurer, shared address, shared management company, and transaction timing create a factual predicate to examine whether common operational control existed.

A Second Shared Treasurer

The Boland pattern is not unique. A parallel structure appears in the Emgage network.

Amin Mitha serves as Treasurer for Emgage Federal PAC — and also for Defend and Advance – NY I.E., one of the IE committees that received money from the PAC.

Emgage Federal PAC contributed $60,000 to NYC Independent Expenditure committees (NYC CFB contribution records):

| Contributor | Recipient | Date | Amount |

|---|---|---|---|

| Emgage Federal PAC (Treasurer: Amin Mitha) | WFP National PAC – NYS IE Committee | 6/17/2025 | $25,000 |

| Emgage Federal PAC (Treasurer: Amin Mitha) | Defend and Advance – NY I.E. (Treasurer: Amin Mitha) | 9/18/2025 | $35,000 |

Same structure as Boland: the same treasurer appears on both the contributor PAC and one of the recipient IE committees. And both IE committees — WFP National PAC and Defend and Advance — spent money supporting Mamdani.

Emgage Action Inc (501(c)(4)) — which ran a phone bank for Mamdani paid for by WFP National PAC – NYS IE — also made $8,593.55 in third-party payments to the same IE committee. (NYC CFB contribution records)

A separate disclosure issue: Emgage Foundation Inc (501(c)(3)) and Emgage Action Inc (501(c)(4)) share the same address (3425 US Highway 98 North, Lakeland, FL 33809), the same Treasurer (Mitha), and the same registered agent — yet both answered “No” on Form 990 Part IV Line 34: “Was the organization related to any tax-exempt or taxable entity?” (Emgage Foundation Form 990 – ProPublica) That answer deserves review against the Form 990 related-organization definitions.

Two separate networks. Two shared treasurers. The same structural pattern.

The “Partners”

The financial overlap isn’t the only connection.

On June 25, 2025, Movement Voter Project published a report celebrating the grassroots effort behind Mamdani’s campaign. They named names: Make the Road Action Inc (501(c)(4)) and Working Families Party were “MVP partners” working “in partnership with” each other.

The report detailed what that partnership looked like: shared volunteers, coordinated phone banks, aligned strategy.

This wasn’t a one-time description. Working Families Party’s own November 9, 2022 memo openly stated: “WFP coordinated a significant grassroots IE table.”

Independent expenditures cannot be coordinated with the candidate or campaign, and New York separately restricts PAC-to-IE transfers under common operational control. Yet WFP openly used the word “coordinated” to describe a grassroots IE table — documenting 400,000 doors knocked in Pennsylvania alone, simultaneous field programs across six battleground states, and systematic IE operations.

Make the Road Action Inc (501(c)(4)) filed Independent Expenditure reports. So did Working Families Party committees. “Independent” means no prohibited coordination with candidates — and under New York law, certain PAC-to-IE relationships are barred when common operational control exists.

The “partnership” language is not proof of Mamdani campaign coordination. Courts have held that ideological alignment, shared goals, and even being “on the same page” are not enough without discussion or negotiation over campaign content, timing, or targeting. But the language does create a factual tension. Organizations publicly celebrating their partnership while filing as independent committees invite scrutiny. At minimum, it warrants examination of what “partnership” meant in practice — and whether it extended to the kinds of strategic discussions or material involvement that trigger coordination rules.

147,000 Doors

The partnership wasn’t just financial. It was boots on the ground.

| Organization | Ground Operations | Source |

|---|---|---|

| Jewish Voice for Peace Action | 80,000 doors | JVP Action Instagram, June 17, 2025 |

| Make the Road Action | 60,000 doors | Movement Voter Project |

| NY Communities for Change | 7,500 doors; 30,000 phone calls | Inside Climate News, July 31, 2025 |

| Working Families Party | 1,000+ volunteers; 100+ canvassing events | Movement Voter Project |

| TOTAL | 147,500+ doors; 30,000+ phone contacts |

All in electoral efforts that benefited Mamdani.

The filings and public records show these organizations were connected through overlapping funding, political partnerships, or field operations tied to the same broader network. Each either endorsed Mamdani or deployed field operations that supported or benefited his candidacy — and all were documented as working together.

NYC Campaign Finance Board records add another data point.

On June 21-22, 2025, Emgage Action ran a virtual phone bank for “Zohran Mamdani for mayor.” The disclosure says it was “Paid for by WFP National PAC – NYS IE.” (NYC Campaign Finance Board IE filings)

The same disclosure lists the IE committee’s top three donors: “Leaders We Deserve PAC, Working Families Party PAC, Make the Road Action Inc (501(c)(4)).”

So Make the Road Action Inc (501(c)(4)) gives money to the IE committee. The IE committee pays for phone banks run by Emgage Action Inc (501(c)(4)). Movement Voter Project documents Make the Road and Working Families as “partners.”

None of this proves Mamdani campaign coordination by itself. But the pattern — shared funding, shared operations, shared “partnership” framing — creates an investigative predicate that regulators should examine.

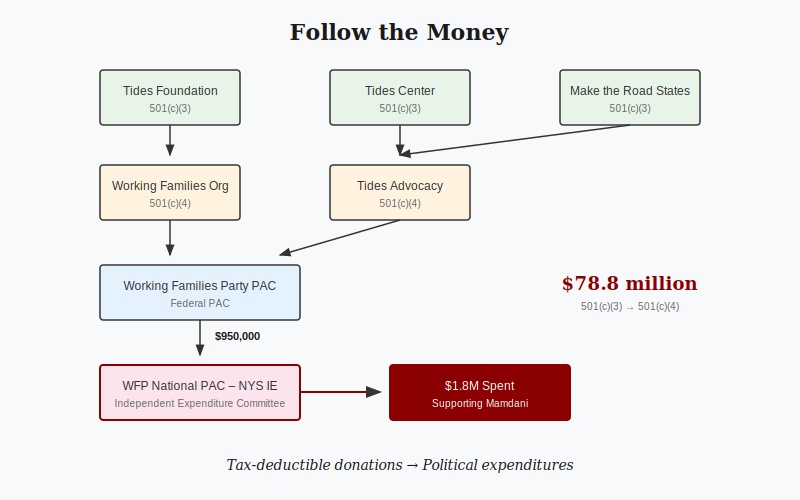

Follow the Money

Where did all this money come from?

Start with Tides Foundation Inc (501(c)(3)). It’s a charity. Donors receive tax deductions for contributing.

Across 2023-2024, Tides Foundation Inc (501(c)(3)) transferred $57,476,616 to Tides Advocacy Inc (501(c)(4)) — $29,312,169 in 2023 and $28,164,447 in 2024. (ProPublica Nonprofit Explorer – Tides Foundation Inc Form 990 Schedule I)

Tides Advocacy Inc (501(c)(4)) is an advocacy organization that engaged in political activity.

That’s $57 million moving from a tax-deductible charity to a 501(c)(4) that subsequently made political expenditures. The unanswered question is whether any charitable funds were restricted, earmarked, commingled, or functionally converted into campaign intervention.

But that’s just one piece.

Tides Foundation Inc (501(c)(3)) also sent $7.8 million directly to Working Families Organization Inc (501(c)(4)) between 2023 and 2024.

Tides Center Inc (501(c)(3)) added another $13,439,545 to Tides Advocacy Inc (501(c)(4)).

Make the Road States Inc (501(c)(3)) contributed $100,000 more.

Total 501(c)(3)-to-501(c)(4) transfers identified: $78,826,027.

| Conversion Pathway | 2023 | 2024 | Total |

|---|---|---|---|

| Tides Foundation Inc (501(c)(3)) → Tides Advocacy Inc (501(c)(4)) | $29,312,169 | $28,164,447 | $57,476,616 |

| Tides Center Inc (501(c)(3)) → Tides Advocacy Inc (501(c)(4)) | $343,753 | $13,095,792 | $13,439,545 |

| Make the Road States Inc (501(c)(3)) → Tides Advocacy Inc (501(c)(4)) | — | $100,000 | $100,000 |

| Tides Foundation Inc (501(c)(3)) → Working Families Organization Inc (501(c)(4)) | $4,555,657 | $3,254,209 | $7,809,866 |

| Total 501(c)(3) → 501(c)(4) Conversions | $34,211,579 | $44,614,448 | $78,826,027 |

Where Did the Tides Network Get Its Money?

Foundation to Promote Open Society (501(c)(3)) and Open Society Institute (501(c)(3)) — George Soros’s primary 501(c)(3) charitable vehicles — made documented grants totaling $11,770,550 to Tides Foundation Inc (501(c)(3)) and Tides Center Inc (501(c)(3)) across 2023-2024.

| Source | Recipient | 2023 | 2024 | Source Document |

|---|---|---|---|---|

| Foundation to Promote Open Society (501(c)(3)) | Tides Foundation Inc (501(c)(3)) | $6,435,550 | $1,350,000 | Form 990-PF, Part XIV |

| Foundation to Promote Open Society (501(c)(3)) | Tides Center Inc (501(c)(3)) | $2,085,000 | $550,000 | Form 990-PF, Part XIV |

| Open Society Institute (501(c)(3)) | Tides Foundation Inc (501(c)(3)) | — | $1,350,000 | Form 990, Sch I |

| Total Soros 501(c)(3) → Tides Network | $8,520,550 | $3,250,000 |

Separately, Open Society Policy Center (501(c)(4)) made five grants totaling $4,100,000 directly to Tides Advocacy Inc (501(c)(4)) in 2024 — including a $3,000,000 grant explicitly referencing the “Electoral Justice Project” on the face of the Schedule I. (Open Society Policy Center (501(c)(4)) 2024 Form 990, Schedule I, Lines 177-181)

The money trail runs from Soros 501(c)(3) entities → Tides network 501(c)(3) charities → Tides Advocacy Inc (501(c)(4)) → downstream 501(c)(4) organizations and PACs → IE committees → expenditures supporting one candidate.

Now follow where it went.

Tides Advocacy Inc (501(c)(4)) distributed funds to organizations at the center of this story:

| Recipient | Amount (Two-Year) |

|---|---|

| Working Families Organization (501(c)(4)) | $1,220,173 |

| Make the Road Action (501(c)(4)) | $350,000 |

| Center for Popular Democracy Action Fund (501(c)(4)) | $250,000 |

| Emgage Action (501(c)(4)) | $150,000 |

| WFP National PAC / Working Families Party (527) | $141,000 |

| Jewish Voice for Peace Action (501(c)(4)) | $100,000 |

| Total to Mamdani-endorsing organizations | $2,211,173 |

Working Families Organization Inc (501(c)(4)) then transferred $2 million to Working Families Party PAC on December 9, 2024. (FEC Form 3X, Schedule A, Transaction ID SA17.213711)

Working Families Party PAC transferred $950,000 to the IE Committee on October 22, 2025.

The IE Committee spent $1.8 million on “independent” expenditures for Mamdani.

The money trail runs from tax-deductible donations through 501(c)(3) charities to 501(c)(4) advocacy organizations to PACs to an IE committee to expenditures supporting one candidate.

If charitable funds were earmarked, restricted, or functionally used to support political expenditures, the chain becomes relevant to both tax and election-law review.

The Penny-Perfect Red Flag

If the money trail shows the flow, one transaction shows the precision.

| Direction | Amount | Purpose |

|---|---|---|

| Make the Road Action Inc (501(c)(4)) → WFP National PAC | $45,697.14 | Contribution |

| WFP National PAC → Make the Road Action Inc (501(c)(4)) | $45,697.14 | In-kind: “Phone Bank” |

Same day. Same amount. To the penny.

At minimum, this is a forensic red flag. It may reflect the reporting mechanics of an in-kind contribution, a reimbursement arrangement, or a circular transaction. The only way to know is to examine the underlying invoices, bank records, reimbursement records, and internal communications.

Dollar-for-dollar same-day entries are difficult to dismiss without underlying documentation. This is not the kind of pattern a regulator should ignore.

The Personnel Connection

One more piece.

On March 19, 2026, Mayor Mamdani appointed Renita Francois as Deputy Mayor for Community Safety. (NYC Mayor’s Office)

The appointment matters because Francois previously appears in Tides Advocacy Inc’s (501(c)(4)) 2023 Form 990 as Chief Program Officer, with reportable compensation of $155,036. (ProPublica Nonprofit Explorer – Tides Advocacy Inc Form 990)

City Hall’s announcement described her most recent role as Chief Strategy Officer and Chief Program Officer at Beyond Impact — the organization formerly known as Tides Advocacy, which rebranded in February 2026 — where she “oversaw millions of dollars in grants and managed relationships with political leaders and community organizations.” (NYC Mayor’s Office)

The personnel integration runs deeper than one appointment. Janiece Evans-Page serves as CEO of Tides and sits on the board of Tides Advocacy (501(c)(4)). (Tides Foundation) The entities operate under documented cost-sharing agreements covering shared staff, office space, and programmatic expenses. (2023 Deloitte Audit)

The Tides Advocacy Inc (501(c)(4)) connection is documented in public tax filings. The City Hall language about overseeing millions belongs to her later Beyond Impact role. Both facts warrant scrutiny, but they should not be collapsed into one claim.

What is clear: a person who held a senior position at Tides Advocacy Inc (501(c)(4)) during the years it received tens of millions from 501(c)(3) charities and distributed millions to organizations supporting Mamdani is now Deputy Mayor in his administration.

The Legal Framework

New York Election Law provides the most direct avenue for scrutiny.

Under § 14-107-a, PACs cannot contribute to IE committees under “common operational control” — defined as the same individuals exercising actual and strategic control over day-to-day affairs, or employees communicating about strategic operations.

Under § 14-126, knowing and willful violations of § 14-107-a can trigger civil penalties. Criminal exposure may arise only if additional facts show conduct falling within § 14-126’s separate felony provision, including coordination of unauthorized committee activity for the purpose of evading contribution limits.

Federal election law may also apply to the extent federally registered committees, federal accounts, conduit contributions, or federal reporting obligations are implicated. Under 11 C.F.R. § 109.21, a federal coordinated communication can satisfy the conduct prong through material involvement, substantial discussion, request or suggestion, or certain common-vendor relationships; if the payment and content prongs are also met, the communication is treated as an in-kind contribution.

Tax law becomes relevant if 501(c)(3) charitable funds were functionally converted into political expenditures. Under IRC § 4955, when 501(c)(3) organizations make transfers that constitute political expenditures — including transfers to 501(c)(4) organizations that then deploy those funds politically — the 501(c)(3) faces excise taxes of 10% initially, rising to 100% if not corrected.

The Predictable Defenses

Defenders of this network will offer familiar arguments.

They will say Mike Boland is a “ministerial treasurer” — a compliance professional who signs checks but has no strategic input. They will cite the 2010 federal and state investigations into WFP’s “Data and Field Services” that closed without charges because investigators couldn’t prove the strategic wall had been breached.

They will say the penny-perfect $45,697.14 transaction reflects strict accounting standards, not circular movement — that if Make the Road Action Inc (501(c)(4)) pre-paid a vendor and WFP later bought in, the reimbursement had to be recorded immediately under CFB’s 24-hour reporting rule.

They will say “partnership” is movement rhetoric, not legal coordination — that bragging about a “coordinated grassroots table” is political puffery, not evidence of material coordination under Vermont Right to Life standards.

They will say Renita Francois was a “seasoned city administrator” rehired after a gap year in nonprofits — not a political operative being rewarded.

But firewalls are only as strong as the people who maintain them. When the same names appear on every floor of the building — when organizations publicly celebrate their “partnership” while filing certifications of independence — the burden of explanation should shift from the public to the spenders.

And there is one defense they cannot offer: NYC Independent Expenditure spenders must certify under penalty of perjury that they did not coordinate. If WFP’s own 2022 memo says it “coordinated a significant grassroots IE table,” that language becomes a focal point for examining whether later independence certifications were accurate.

The Questions

Six questions about potential Mamdani campaign coordination emerge from the public record:

1. When Mike Boland serves as treasurer for both the PAC that gave $950,000 and the IE committee that spent it — operating from the same address with the same management company — does that constitute “common operational control” under New York law?

2. When Movement Voter Project documents organizations working “in partnership” — what did that partnership entail, and did it extend to strategic discussions or material involvement in campaign activity?

3. When 147,500 doors are knocked by organizations funded through the same network, endorsed the same candidate, and were documented as “partners” — should regulators examine whether those operations were truly independent?

4. When $45,697.14 is recorded moving one direction and $45,697.14 is recorded moving back the same day — what do the underlying records show?

5. When nearly $79 million flows from tax-deductible charities through advocacy organizations to political committees — were any charitable funds restricted, earmarked, or functionally converted into campaign activity?

6. When a person who held a senior position at the network’s advocacy hub becomes Deputy Mayor for the candidate who benefited — does that relationship warrant examination?

What Happens Now

The public filings create a clear investigative trail for examining potential Mamdani campaign coordination.

This warrants examination by:

- NYC Campaign Finance Board — Independent expenditure reporting, coordination, in-kind valuation, disclosure

- New York State Board of Elections — Common operational control under Election Law § 14-107-a; civil penalties under § 14-126; potential criminal exposure only if additional facts support § 14-126’s felony provisions

- New York Attorney General Charities Bureau — Charitable asset diversion and nonprofit governance

- Internal Revenue Service — IRC § 501(c)(3), § 501(c)(4), and § 4955 issues

- FEC / DOJ — To the extent federally registered committees, federal funds, conduit contributions, or FECA reporting obligations are implicated

This article does not conclude that crimes occurred. It documents a public record that raises serious questions.

The question is not whether any single filing proves coordination by itself. The question is why so many supposedly independent entities kept showing the same treasurers, funders, vendors, partners, field operations, and matching transactions — while spending to elect the same candidate.

The facts are strong enough that regulators should have to examine whether Mamdani campaign coordination occurred — not why anyone is asking.

Written by Sam Antar | Forensic Accountant & Fraud Investigator

I have written extensively about the tax-exempt funding network behind Zohran Mamdani’s campaign — the tax issues, the 501(c)(3)-to-501(c)(4) conversions, the charitable-to-political pipelines. That work continues. But the public filings also raise a separate set of questions: not just where the money came from, but how it was spent — and whether the organizations that spent it were as independent as they claimed.

All sources are publicly available through FEC filings, NYC Campaign Finance Board records, IRS Form 990 data, and the organizations’ own published statements.

Follow @SamAntar on X

© 2026 Sam Antar. All rights reserved.