For the past year I have documented how charitable foundations funded by George Soros move tax-deductible money into political activity through a chain of related tax-exempt organizations. At the point where that chain crosses the line between charity and politics sits a single 501(c)(4): Tides Advocacy Inc (501(c)(4)) — now rebranded “Beyond Impact.” It is the point where money from 501(c)(3) charitable entities — given by donors who claimed federal tax deductions — is received by a 501(c)(4) that engages in political campaign spending, the kind of spending the charitable entities themselves are barred from undertaking. That structure raises questions about sourcing and segregation that the IRS would have to resolve.

Over fiscal years 2023 and 2024, according to its filed Forms 990 and audited financial statements, Tides Advocacy (501(c)(4)) drew approximately 45% of its two-year revenue — tens of millions of dollars — from five affiliated Tides 501(c)(3) charitable entities (Tides Foundation Inc, Tides Center Inc, Tides Network, Tides Inc, and Tides Two Rivers Fund — hereinafter the “Tides 501(c)(3) entities”). Over the same two years it reported $22.2 million in political campaign expenditures and distributed $2.21 million to organizations that endorsed Zohran Mamdani for mayor of New York.

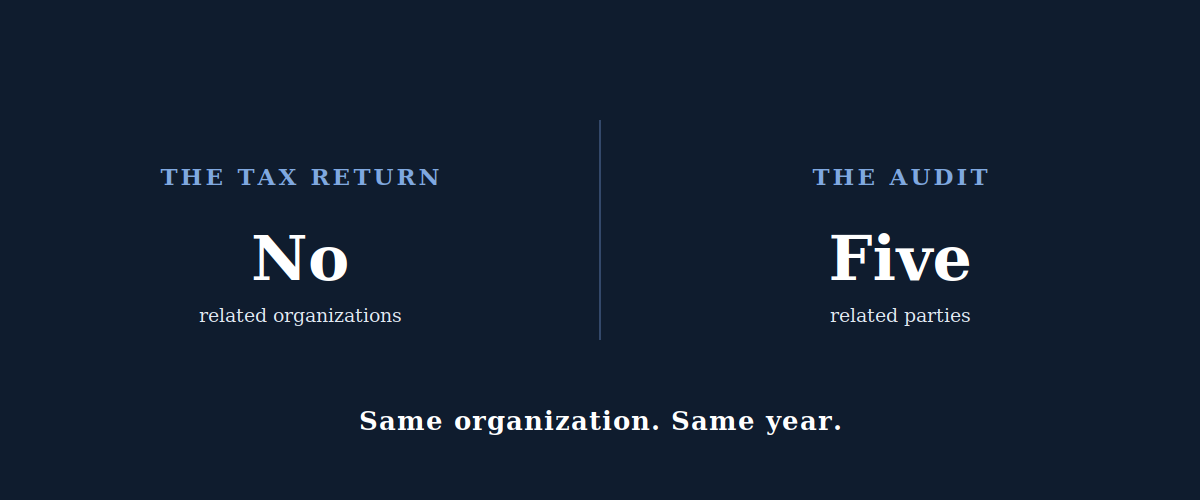

On its 2024 federal tax return, signed under penalties of perjury, Tides Advocacy (501(c)(4)) reported that it had no related organizations. Its audited financial statements covering the same fiscal year, signed by Baker Tilly US LLP, named five Tides 501(c)(3) entities as related parties and disclosed shared employees, shared facilities, shared overhead, and $40.6 million in two-way transactions for that year alone. The two documents describe the same relationships, for the same fiscal year, using two different definitional frameworks — and the IRS framework is the one that goes unsatisfied on the face of the return. A financial-statement audit identifies “related parties” under accounting standards; the Form 990’s Schedule R identifies “related organizations” under the Internal Revenue Code’s control and support tests. Those are not identical regimes.

But the audit does not merely apply a broad accounting label — it describes shared employees, shared facilities, shared overhead, common officers, and a parent that is the sole member of the affiliated entities. Those are the very facts the Schedule R tests turn on. The apparent inconsistency is therefore not a matter of definitions alone; it is a question the IRS resolves by applying its own tests to the relationships the auditor describes.

On October 28, 2025, I published an investigative article naming Tides Advocacy (501(c)(4)) and documenting its role in that network. Three months later, the organization rebranded itself as “Beyond Impact.” The public disclosure that had described it as “an affiliate of Tides Network, a 501(c)(3) charitable organization” disappeared. The board page no longer listed anyone from Tides. The name “Tides Advocacy (501(c)(4))” was removed from the organization’s own public-facing language, per archived captures.

This article documents that conduct in the organizations’ own federal filings, their own audited financial statements, and the archived record of their own websites. It raises four questions those documents pose. It does not assert their answers — that is for the Internal Revenue Service to determine.

The Entities in This Report

The organizations examined here share the “Tides” name and a common operational structure, which can make them easy to confuse. They fall into two tax categories, and that distinction is the center of this report. The following table identifies each entity, its tax status, and its role.

| Entity | Tax status | Role in this report |

|---|---|---|

| The 501(c)(4) — social welfare organization (may engage in political activity) | ||

| Tides Advocacy Inc (now “Beyond Impact”) | 501(c)(4) | The social welfare organization at the center of this report. Receives charitable money from the Tides 501(c)(3) entities; reports political campaign expenditures. |

| The Tides 501(c)(3) entities — charitable organizations (barred from political campaign intervention; audited together by Deloitte & Touche LLP) | ||

| Tides Foundation Inc | 501(c)(3) | Charitable entity. Largest source of funds to Tides Advocacy. |

| Tides Center Inc | 501(c)(3) | Charitable entity. Second source of funds to Tides Advocacy; recipient of the federal awards in the consolidated audit. |

| Tides Network | 501(c)(3) | Charitable entity. The sole member and board-appointer of the other Tides 501(c)(3) entities; absorbs their operating costs and management salaries. |

| Tides Inc | 501(c)(3) | Charitable entity within the consolidated network. |

| Tides Two Rivers Fund | 501(c)(3) | Charitable entity within the consolidated network. |

The five 501(c)(3) entities — Tides Foundation, Tides Center, Tides Network, Tides Inc, and Tides Two Rivers Fund — are referred to collectively in this report as the “Tides 501(c)(3) entities.” They are audited together by Deloitte & Touche LLP in a single consolidated financial statement. Tides Advocacy (501(c)(4)) is audited separately by Baker Tilly US LLP. The line between the 501(c)(3) entities and the 501(c)(4) is the line federal tax law draws between charitable money and political money — and it is the line this report examines.

Why This Matters

Since 2025, my reporting has examined a network of tax-exempt organizations funded through George Soros–affiliated charitable foundations, in which 501(c)(3) charitable dollars were converted into 501(c)(4) political activity through a series of intermediary transfers. The Tides entities sit at the center of that network as the primary intermediaries — and Tides Advocacy Inc (501(c)(4)), the network’s 501(c)(4) arm, is the critical conversion point: the entity where charitable money received from 501(c)(3) sources meets the political campaign expenditures the law forbids those 501(c)(3) sources from making directly. The earlier reporting documented the flows; this article documents how the federal disclosure framework that should make those flows visible was not used to disclose them.

The legal stakes turn on a hard line. Federal tax law separates 501(c)(3) charitable organizations from 501(c)(4) social welfare organizations. Donations to a 501(c)(3) are tax-deductible; the charity is barred from political campaign intervention. Donations to a 501(c)(4) are not deductible; the organization may engage in political activity. The IRS Schedule R related-organization disclosure framework is one of the principal tools the federal government uses to make money flowing across that line examinable on the face of a Form 990.

The Disclosure That Polices the Boundary

That is precisely the disclosure that is missing here. The relationships the Tides network does disclose on Schedule R are the inter-501(c)(3) ones — the relationships that do not bear on a charitable-to-political conversion analysis. The relationship none of the network’s Form 990s disclose is the 501(c)(3) ↔ 501(c)(4) relationship between the Tides charitable entities and Tides Advocacy (501(c)(4)) — the one relationship that does. The pattern is consistent: across the network’s filings, the relationships that are disclosed are the inter-501(c)(3) ones, and the relationship that is not disclosed is the 501(c)(3)–501(c)(4) one — the line federal tax law uses to separate charitable money from political money. Whether that reflects a correct application of Schedule R’s tests or an omission is a question for the IRS.

Why the Conflict Is Not a Technicality

The stakes are concrete. Approximately 45% of Tides Advocacy (501(c)(4))’s revenue came from 501(c)(3) charitable sources over two years, while the organization spent $22.2 million on political campaign activity. Its own auditor disclosed that it shares employees, facilities, and overhead with the Tides 501(c)(3) entities.

When the charitable operation and the political operation run on the same staff, in the same offices, under shared cost allocations, the question of whether charitable dollars subsidized political activity is concrete rather than abstract. Shared services can be entirely permissible when properly costed and allocated; whether they were is a question that requires the timekeeping, cost-sharing, and allocation records the public file does not contain. What the public file does show is that the relationship which would frame that question is not disclosed on Schedule R.

The conflict between the Form 990 and the audit report is therefore not a paperwork technicality. It is an examination-grade discrepancy on the exact relationship that matters most to the charitable-to-political conversion question — and it sits inside a documented pattern of the organization removing, from its own public-facing materials, the language that once described that relationship.

Substance Over Form

There is a settled tax-law principle that governs exactly this kind of conflict between what a form says and what an organization does. It is called substance over form. Federal tax law examines how organizations actually operate — the substance — rather than how their legal structures are characterized on paper — the form. A “No” in a disclosure box does not control if the operational reality is a related-organization relationship.

When an organization’s own independent auditor reports that it shares employees, shares facilities, shares overhead, and conducts tens of millions of dollars in transactions with the five Tides 501(c)(3) entities, the substance of the relationship is documented — by the organization’s own auditor — regardless of how the box on the Form 990 was checked. Tax law looks at what organizations do, not only at what their filings say. That is why pointing to the form does not end the matter: under that principle, the Form 990 answer does not close the inquiry — it is tested against the operational facts.

Substance does not by itself convert an entity into a Schedule R “related organization”; that still turns on the IRS’s defined control and support tests. But the operational facts the auditor describes — shared staff, shared facilities, common officers, a sole-member parent — are precisely the inputs those tests evaluate.

Investigative Background

Beginning in June 2025, I published a series of investigative articles at WhiteCollarFraud.com examining the Tides network and charitable-to-political funding flows. The findings below are drawn entirely from public federal information returns, publicly filed independent audit reports, and archived public web pages.

The Money: Charitable In, Political Out

Over fiscal years 2023 and 2024, Tides Advocacy (501(c)(4)) received approximately $71 million from Tides 501(c)(3) charitable entities — primarily Tides Foundation Inc (501(c)(3)) ($57.5 million) and Tides Center Inc (501(c)(3)) ($13.4 million). Donors to those 501(c)(3) entities received federal charitable tax deductions under IRC §170.

Over the same two years, Tides Advocacy (501(c)(4)) reported $22,209,240 in political campaign expenditures on Schedule C of its Form 990 ($5.4 million in 2023; $16.8 million in 2024). Its own Baker Tilly–audited financial statements disclosed $2,960,686 in IRC §527(f)(1) tax for 2024 — a tax that 501(c) organizations pay on their own political spending.

One point deserves clarity, because it is easy to misread. The §527(f)(1) tax is not a payment that makes the funding structure permissible. Paying it does not, by itself, cure any upstream sourcing question on the charitable side; it primarily corroborates that political expenditures occurred at scale. It is a tax a 501(c)(4) pays on the income it devotes to political activity — in effect, the price a social welfare organization pays for spending on politics.

Tides Advocacy (501(c)(4)) paying it does not “cure” anything. It confirms only one fact: that Tides Advocacy (501(c)(4)) engaged in political campaign spending at substantial scale, which the organization is permitted to do as a 501(c)(4). That is precisely why this article treats the $2.96 million figure as corroboration that the political activity occurred — not as a violation, and not as a defense.

The conversion question lives on the other side of the boundary. It concerns the 501(c)(3) charitable entities — Tides Foundation (501(c)(3)) and Tides Center (501(c)(3)) — and the donors who took deductions: whether tax-deductible charitable dollars improperly funded political campaign activity, whether donors claimed charitable deductions for what became political spending, and whether the cross-boundary relationship was disclosed where federal law requires it. A 501(c)(4) paying tax on its own political spending answers none of those questions. Paying the tax on the downstream political activity does not make it permissible for upstream charitable money to have funded that activity, or for donors to have deducted it. Those are separate taxpayers, separate sections of the tax code, and separate questions — and they are the questions this record raises.

Source: 2023 and 2024 Tides Foundation (501(c)(3)) (ProPublica) and Tides Center (501(c)(3)) (ProPublica) Form 990, Schedule I; 2023 and 2024 Tides Advocacy (501(c)(4)) Form 990, Schedule C (ProPublica); 2024 Tides Advocacy (501(c)(4)) Audited Financial Statements, Note 3 (Baker Tilly US LLP, signed July 15, 2025).

Where the Political Money Went

Of those political distributions, $2,211,173 over the two-year period went to organizations that endorsed Zohran Mamdani for NYC mayor.

| Year | Recipient | Amount |

|---|---|---|

| 2023 | Working Families Organization Inc (501(c)(4)) | $295,173 |

| 2023 | WFP National PAC (527) | $135,000 |

| 2023 | Jewish Voice for Peace Action Inc (501(c)(4)) | $100,000 |

| 2024 | Working Families Organization Inc (501(c)(4)) | $925,000 |

| 2024 | Make the Road Action Inc (501(c)(4)) | $350,000 |

| 2024 | Center for Popular Democracy Action Fund Inc (501(c)(4)) | $250,000 |

| 2024 | Emgage Action Inc (501(c)(4)) | $150,000 |

| 2024 | Working Families Party Inc (527) | $6,000 |

| Total | $2,211,173 |

Source: 2023 and 2024 Tides Advocacy (501(c)(4)) Form 990, Schedule I and Schedule C (ProPublica).

The Leadership Overlap

The same individual served simultaneously as a Director of Tides Advocacy Inc (501(c)(4)) and as Principal Officer / CEO of three of the 501(c)(3) entities the organization’s own auditor names as related parties.

| Person | Tides Advocacy | Tides Network | Tides Center | Tides Foundation |

|---|---|---|---|---|

| Janiece Evans-Page | Director | Director / CEO | Principal Officer / CEO | Principal Officer / CEO |

The Tides Foundation (501(c)(3)) 2023 Form 990, Schedule O, states it directly: “Janiece Evans-Page, Suneela Jain, Holden Lee, and James Lum were officers of Tides Foundation and provide services to Tides Foundation through that organization’s cost sharing agreement with Tides Network.”

Source: 2023 Form 990, Part VII and Schedule O, for each entity.

The Rebrand

On October 28, 2025, I published an investigation that directly named Tides Advocacy (501(c)(4)). The Wayback Machine captured the organization’s FAQ page — still describing Tides Advocacy (501(c)(4)) as “an affiliate of Tides Network, a 501(c)(3) charitable organization” — intact on January 1, January 2, and January 11, 2026. On February 1, 2026, the organization rebranded as “Beyond Impact.” By February 2026, the affiliate disclosure was gone, the board page no longer listed Tides leadership, and the name “Tides Advocacy (501(c)(4))” had been removed from the public-facing site, per archived captures.

Source: Internet Archive Wayback Machine captures of tidesadvocacy.org, January 2026; beyondimpact.org, February–May 2026; tidesadvocacy.org/about/contact, January 2, 2026 (three disclosed mailing addresses); beyondimpact.org contact page, May 2026 (one disclosed mailing address — the West Hollywood PMB).

Two Auditors, One Network, Split Along the Same Line

The Tides network is audited by two different firms, and the split runs exactly along the 501(c)(3) / 501(c)(4) boundary. Deloitte & Touche LLP audits the consolidated Tides 501(c)(3) entities — Tides Network (501(c)(3)), Tides Center (501(c)(3)), Tides Foundation (501(c)(3)), Tides Inc (501(c)(3)), and Tides Two Rivers Fund (501(c)(3)) — in a single consolidated financial statement signed July 8, 2025. Baker Tilly US LLP separately audits Tides Advocacy, the 501(c)(4), signing its report one week later on July 15, 2025. Tides Advocacy (501(c)(4)) is not consolidated into the Deloitte statements, and the Deloitte audit does not name it.

That, by itself, is unremarkable: Tides Advocacy is a 501(c)(4), so it would not appear inside a consolidated 501(c)(3) audit. The forensically significant point is what the two audits show when read together.

The Deloitte audit describes a 501(c)(3) structure that is fully centralized. In its own words: “Network is the sole member and appoints board members of Center, Foundation, TINC, and TTRF. Network also supports their operations and strategy. Network oversees aligned direction and policy orientation for and has economic interest in all of Tides Organizations. All direct and indirect costs of supporting services of Tides Organizations, including management salaries, are incurred within Network.” One entity owns the others, appoints their boards, sets their direction, and absorbs all of their operating costs and management salaries.

That description is not a one-year characterization. The same integrated-structure language appears, word for word, in two separately signed consolidated audits — the one covering fiscal year 2023, signed May 28, 2024, and the one covering fiscal year 2024, signed July 8, 2025. Two audit cycles, two signing dates, the same description of a single centralized enterprise.

The Baker Tilly audit then extends that same integrated structure across the boundary. It states that Tides Advocacy (501(c)(4)) “shares certain administrative expenses with the Entities, including use of the Entities’ employees, facilities, and a portion of overhead costs of the Entities” — naming the same five Tides 501(c)(3) organizations. Two independent firms, engaged separately, auditing opposite sides of the 501(c)(3) / 501(c)(4) line, describe a single operationally integrated enterprise: one where the 501(c)(3) network incurs all the costs and supplies the staff, and the 501(c)(4) uses those same employees, facilities, and overhead.

Notwithstanding the separate audits, both reports, read together, describe extensive operational integration across the entities. And none of that cross-boundary integration — the shared employees, the shared facilities, the shared overhead that Baker Tilly names — appears on any Tides entity’s Schedule R as a related-organization relationship between the 501(c)(3) network and Tides Advocacy (501(c)(4)).

Source: 2023 and 2024 Tides Organizations Consolidated Financial Statements, Note 1 (Deloitte & Touche LLP, signed May 28, 2024 and July 8, 2025); 2024 Tides Advocacy (501(c)(4)) Audited Financial Statements (Baker Tilly audit), Note 12 (signed July 15, 2025).

Question One: The Form 990 and the Audit Report Describe the Same Relationships Under Conflicting Standards

For the fiscal year ending December 31, 2024, Tides Advocacy (501(c)(4)) made two formal attestations about its relationships to other entities.

The Form 990, signed under penalties of perjury, Part IV Line 34: “No” related organizations. No Schedule R filed.

The Baker Tilly US LLP audit, covering the same fiscal year, signed July 15, 2025, Note 12 (Related-Party Transactions), opens:

“The Organization has relationships with Tides Center, Tides Foundation, Tides Network, Tides, Inc., and Tides Two Rivers Fund (the Entities).”

Note 12 then discloses $40.6 million in two-way transactions with those five Tides 501(c)(3) entities for 2024 alone, plus shared employees, shared facilities, and shared overhead. Across both fiscal years, the audit-disclosed two-way flow between Tides Advocacy (501(c)(4)) and the five Tides 501(c)(3) entities totals approximately $74.7 million. None of it appears on any Tides network Schedule R for either year.

| Year | Tides Advocacy Payments to the Tides 501(c)(3) Entities | Tides Advocacy Receipts from the Tides 501(c)(3) Entities |

|---|---|---|

| 2024 | $1,702,370 | $38,868,234 |

| 2023 | $1,273,981 | $32,883,781 |

| Two-Year Total | $2,976,351 | $71,752,015 |

The two documents describe the same entities, the same fiscal year, and the same relationships. One reports them as related parties sharing employees and facilities. The other reports no related organizations at all. Both were prepared for the same organization. Both are in the public record.

Source: 2024 Tides Advocacy (501(c)(4)) Form 990, Part IV Line 34 (ProPublica); 2024 Tides Advocacy (501(c)(4)) Audited Financial Statements, Note 12 (Baker Tilly US LLP).

Question Two: Why Does Every Tides Form 990 Exclude the Same Relationship?

The disclosure gap is not confined to Tides Advocacy (501(c)(4))’s own filing. Four other Form 990s in the Tides network for the same fiscal year — Tides Foundation (501(c)(3)), Tides Center (501(c)(3)), Tides Network (501(c)(3)), and Tides Inc (501(c)(3)) — each answered “Yes” to Part IV Line 34, filed Schedule R, named only other Tides 501(c)(3) entities as related organizations, and did not name Tides Advocacy (501(c)(4)) under any code. (The fifth Tides 501(c)(3) entity named in the audit, Tides Two Rivers Fund, is itself named as a related organization on those Schedule R filings; its own Schedule R is not separately analyzed here. Notably, each of these four filers names the others as related 501(c)(3) organizations — yet none extends that disclosure to the 501(c)(4).)

| Entity | Tax Status | 2024 Form 990 Part IV, Line 34 | Schedule R Filed? | Names Tides Advocacy as a Related Org on Schedule R? |

|---|---|---|---|---|

| Tides Foundation Inc | 501(c)(3) | “Yes” | Yes | No |

| Tides Center Inc | 501(c)(3) | “Yes” | Yes | No |

| Tides Network | 501(c)(3) | “Yes” | Yes | No |

| Tides Inc | 501(c)(3) | “Yes” | Yes | No |

| Tides Advocacy Inc / Beyond Impact | 501(c)(4) | “No” | No | N/A — did not file Schedule R |

Five Form 990s in one network for one fiscal year. The auditor names Tides Advocacy (501(c)(4)) as part of the related-party group. None of the five Form 990s place it there. The exclusion is symmetric: every filing in the network treats the 501(c)(3) ↔ 501(c)(4) boundary as the one relationship that does not get disclosed on Schedule R.

Tides Advocacy (501(c)(4)) filed zero Schedule R relationship disclosures for five consecutive years (2019–2023), as I documented in prior reporting, and continued the same non-disclosure for 2024 — while its own audited financial statements named five related parties and disclosed tens of millions of dollars in two-way flows each year. The relationships that the network does disclose on Schedule R (inter-501(c)(3)) are not the relationships material to a charitable-to-political conversion examination. The relationship that the network does not disclose (501(c)(3) ↔ 501(c)(4)) is the one that is.

Source: 2024 Form 990, Part IV Line 34 and Schedule R Parts II and IV, for Tides Foundation (501(c)(3)) (ProPublica), Tides Center (501(c)(3)) (ProPublica), Tides Network (501(c)(3)) (ProPublica), Tides Inc (501(c)(3)) (ProPublica), and Tides Advocacy (501(c)(4)) (ProPublica).

Question Three: Why Does Tides Advocacy File From an Address 380 Miles From Its Operations?

The five Tides 501(c)(3) entities named in the Baker Tilly audit all report their 2024 Form 990 address as 1012 Torney Avenue, San Francisco, CA 94129.

Tides Advocacy (501(c)(4)) reports its 2024 Form 990 address as 8605 Santa Monica Boulevard PMB 771982, West Hollywood, CA 90069 — a Private Mailbox suite at a Commercial Mail Receiving Agency, approximately 380 miles south of the operational location its own audit describes when it discloses that Tides Advocacy (501(c)(4)) shares the five 501(c)(3) entities’ facilities.

The phone number on the same 2024 Form 990 is (415) 561-6328. Area code 415 is the San Francisco Bay Area — consistent with operations at 1012 Torney Avenue, not with a West Hollywood mailing address.

The address divergence extends further than the Form 990 alone. The Internet Archive captured the Tides Advocacy (501(c)(4)) contact page on January 2, 2026 — the same period the organization was still operating under its original name. That page disclosed not one but three distinct mailing addresses, none of which matches the 1012 Torney Avenue address its own auditor associates with its operations:

- Postal Mail: 8605 Santa Monica Blvd, PMB 771982, West Hollywood, CA 90069 — the same Private Mailbox address reported on the Form 990

- Finance Remittance Mail: PO Box 889381, Los Angeles, CA 90088-9381

- Physical Address for Finance Express Delivery Services: Lockbox Services Box #0399381, Tides Advocacy, 3440 Flair Drive, El Monte, CA 91731

Three Southern California mailing addresses — West Hollywood, Los Angeles, and El Monte — none of which aligns with the San Francisco Bay Area operational location the Baker Tilly audit describes. The sole public-facing identifier that points to the Bay Area is the (415) 561-6328 phone number. The divergence is sustained across both the 2023 and 2024 Tides Advocacy (501(c)(4)) Form 990s.

After the February 2026 rebrand, the Beyond Impact (501(c)(4)) contact page continued to disclose the same West Hollywood Private Mailbox — 8605 Santa Monica Blvd, PMB 771982, West Hollywood, CA 90069 — while the two additional Southern California mailing addresses (the Los Angeles finance-remittance PO Box and the El Monte express-delivery lockbox) no longer appeared. The number of disclosed mailing addresses narrowed from three to one, and the one that remained is the same Private Mailbox suite reported on the Form 990 — still approximately 380 miles from the operational location its own auditor associates with the organization.

Source: 2023 and 2024 Form 990 filings for all five 501(c)(3) entities and Tides Advocacy (501(c)(4)); Baker Tilly Note 12; Deloitte & Touche consolidated audit of Tides Organizations, July 8, 2025; Internet Archive Wayback Machine capture of tidesadvocacy.org/about/contact, January 2, 2026; Wayback Machine capture of beyondimpact.org/about/contact, May 26, 2026.

Question Four: Why Does the Tides Network Still Call Tides Advocacy a Partner — Off the Form 990?

The Tides 501(c)(3) network’s own active recruiting page on tides.org — captured May 11, 2026 — includes this text:

“You can apply to open positions at Tides on this page. If you don’t find a fit at Tides, we recommend that you explore openings with our partners, like Tides Advocacy…”

On its public recruiting page, the Tides network identifies Tides Advocacy (501(c)(4)) as a partner. “Partner” on a recruiting page is a colloquial descriptor, not an IRS relationship classification — but it is the organizations’ own characterization of their relationship, made in public, at the same time their federal tax returns identify no such relationship under Schedule R. The relationship is acknowledged in the place that carries no legal disclosure obligation and omitted from the place that does.

Source: tides.org/careers, accessed May 13, 2026.

The Pattern

Read individually, each finding has an innocent explanation available. Read together, they describe a consistent direction.

The affiliate language was public until I named the entity, then disappeared in a rebrand within weeks of an IRS acknowledgment. The auditor names five related parties; not one of the five network Form 990s reflects the cross-boundary relationship. The filing address sits 380 miles from the operations the same filer’s audit describes. The network calls Tides Advocacy (501(c)(4)) a partner on its recruiting page and a stranger on its tax returns. Five consecutive years of zero Schedule R filings preceded the 2024 non-disclosure.

Taken together, these data points point in a consistent direction: the 501(c)(3) ↔ 501(c)(4) relationship does not appear on the filed Schedules R, despite the integration the auditors describe. Whether that reflects a proper application of Schedule R’s tests or a disclosure lapse is for the IRS to determine. What is not in dispute is the surrounding context: approximately 45% of Tides Advocacy (501(c)(4))’s revenue came from those 501(c)(3) sources, and $22.2 million flowed out as political campaign expenditures. With shared employees, shared facilities, and shared overhead disclosed by the organization’s own auditor, whether charitable dollars were adequately segregated from the political operation is a question that turns on cost-allocation, timekeeping, and intercompany records not in the public file — records the IRS can examine.

What the Documents Establish

- Tides Advocacy (501(c)(4))’s 2024 Form 990 reported no related organizations; its 2024 audited financial statements, covering the same fiscal year, named five Tides 501(c)(3) related parties under accounting standards and disclosed $40.6 million in two-way transactions plus shared employees, facilities, and overhead.

- None of the five Form 990s in the Tides network for fiscal year 2024 places Tides Advocacy (501(c)(4)) on Schedule R as a related organization.

- Tides Advocacy (501(c)(4)) received approximately $71 million from Tides 501(c)(3) entities over two years and reported $22.2 million in political campaign expenditures over the same period — approximately 45% of its revenue derived from 501(c)(3) charitable sources.

- Tides Advocacy (501(c)(4)) distributed $2,211,173 over two years to organizations that endorsed Zohran Mamdani for NYC mayor.

- The same individual served as a Director of Tides Advocacy (501(c)(4)) and as Principal Officer / CEO of three of the related 501(c)(3) entities in the same fiscal year.

- The organization’s public affiliate disclosure was intact through January 11, 2026, and gone after the February 2026 rebrand.

- The Tides network’s active recruiting page identifies Tides Advocacy (501(c)(4)) as a partner; no Tides Form 990 identifies it as a related organization.

What the Documents Do Not Establish

- Whether the Schedule R non-disclosure violated the IRS related-organization rules — including whether “common control” or “supporting organization” status exists under the IRS’s defined tests — is a determination for the Internal Revenue Service, applying those tests to the relationships the audit describes. An audit “related party” under accounting standards is not automatically a Schedule R “related organization” under the Internal Revenue Code.

- Whether 501(c)(3) charitable dollars in fact funded political campaign expenditures — the proportionality and the operational integration raise the question, but resolving it requires the cost-allocation records, time records, and intercompany agreements that are not in the public file, and examination authority I do not have.

- Whether the rebrand and the website changes were undertaken for the purpose of distancing the organization from the funding flows — the timeline raises the question; intent is not established by the public record alone.

I published the charitable-to-political funding analysis on October 28, 2025. Three months later, the organization changed its name and removed the language that had described its relationship to the Tides 501(c)(3) network. But the rebrand changed only the name. The 2024 Form 990 still reports no related organizations. The 2024 audit still names five. The Wayback Machine still holds the affiliate disclosure. The recruiting page still calls Tides Advocacy (501(c)(4)) a partner. The documents that raise these four questions are the organizations’ own — and they remain on the public record regardless of what the website says today.

— S.E. Antar

I will update this analysis as new documents become available. I have been wrong before. When I am wrong, I correct it publicly. That is the standard I hold myself to. It should be the standard applied to every organization that signs a federal information return under penalties of perjury.

By Sam E. Antar | Forensic Accountant & Fraud Investigator

Sam Antar is a former CFO of Crazy Eddie who committed securities fraud before cooperating with federal authorities. He has spent over 30 years training the FBI, SEC, and DOJ on fraud detection. He follows the documents, not the politics.

Follow @SamAntar on X

Disclosure: I am a former felon who committed securities fraud at Crazy Eddie before cooperating with federal authorities. I have spent over 30 years as a consultant and educator on fraud detection for the FBI, SEC, DOJ, and other law enforcement agencies. This analysis is based exclusively on public records and the organizations’ own federal information returns and independently audited financial statements. Nothing in this report constitutes a legal conclusion. Where I characterize something as a documented fact, I have linked or cited its primary source. Where I draw an inference, I have said so explicitly.

This article is part of an ongoing investigation into charitable-to-political funding conversions within the Tides network. Previous coverage:

- Did a Tax-Exempt Political Network Help Elect Zohran Mamdani While Certifying It Was Independent? (May 4, 2026)

- How Soros Tax-Exempt Syndicate Laundered Charitable Donations Into Political Support and Ground Operations for Mamdani (October 28, 2025)

© 2026 Sam E. Antar. All rights reserved.