Between 2016 and 2024, three tax-exempt charities in the Arabella Advisors network moved $389,148,524 to two commonly managed 501(c)(4) funds that reported political-campaign expenditures. The five funds — all managed by the for-profit consulting firm Arabella Advisors — share overlapping Washington, D.C. addresses, and in tax year 2024 used the same return preparer. Those two funds reported $453 million in political-campaign spending. And on the federal tax returns where related organizations would be disclosed if the reporting tests are met, no fund discloses a relationship among the five. Taken together, the filings document a sequence from charitable funding into political-campaign spending — and raise the question the prohibition on political intervention by 501(c)(3) charities exists to answer: whether charitable assets were used for political ends.

Each step in that sequence appears on the funds’ own federal filings.

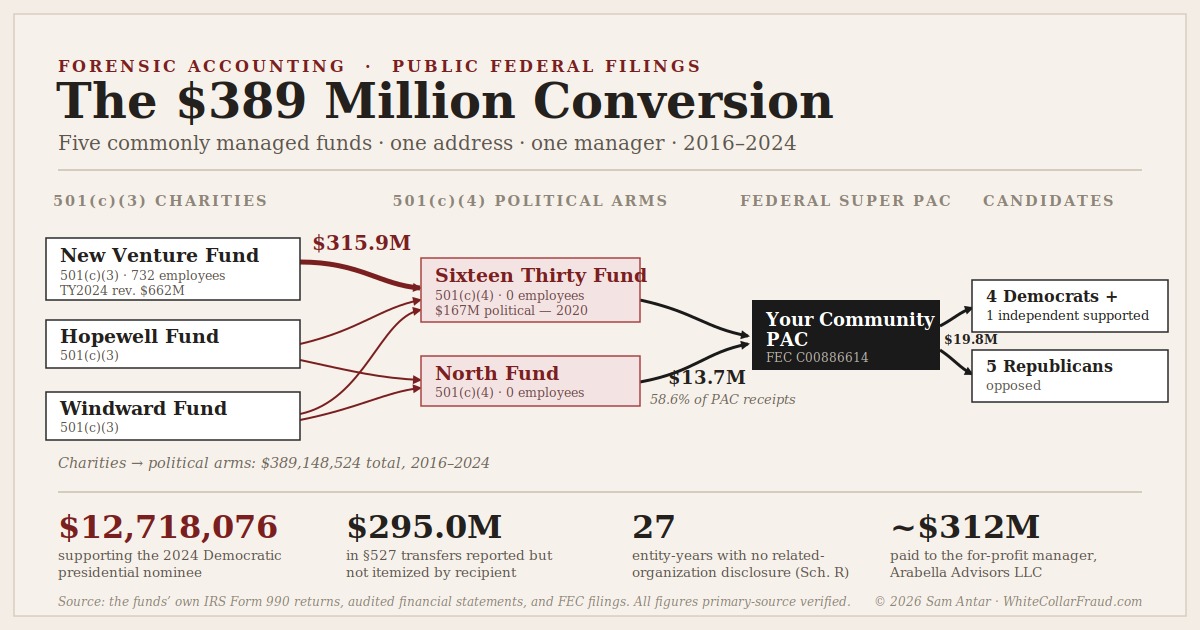

How the Money Moved, in Five Steps

Every link in this sequence appears on the relevant organization’s own federal filing. No single step is unusual by itself — a charity may make grants, a 501(c)(4) may do some political work, and any organization may hire a manager. The questions arise from the combination, and from a principle that runs through federal tax law: what an arrangement is governs over what it is labeled. Tax law calls this substance over form. The labels here say five separate funds, an “unaffiliated” payroll agent, and no relationships to report. The documents support a substance-over-form question: whether five separately incorporated funds functioned, in practice, as one integrated operation.

Step 1 — The charitable source. Three 501(c)(3) charities — New Venture Fund, Hopewell Fund, and Windward Fund — take in tax-deductible contributions. Donors deduct the gift; the charities are barred from intervening in political campaigns.

Step 2 — The transfer across the line. Those charities grant money to the network’s two 501(c)(4) political funds — Sixteen Thirty Fund and North Fund — each grant coded on the charity’s own Schedule I with the recipient’s “501(c)(4)” status. Total, 2016 through 2024: $389,148,524.

Step 3 — The political spending. The two political funds report what they did with the money. On their own Schedule C filings, Sixteen Thirty Fund and North Fund report $453,729,094 in political-campaign expenditures across fifteen entity-years (tax years 2016 through 2024).

Step 4 — The contribution to a super PAC. Through March 31, 2026, those two political funds contributed $13,739,642 to a federal super PAC, Your Community PAC — about 58.6 percent of the committee’s non-memo itemized receipts reviewed ($13,739,642 of $23,449,005).

Step 5 — The spending on candidates. The super PAC reports $19,799,415 in independent expenditures naming federal candidates — including $12,718,076 supporting the 2024 Democratic presidential nominee.

The final link — money spent naming a federal candidate — appears on the recipient committee’s own FEC filings. At each step, the funds involved disclose, on the returns where disclosure is required, no relationship to one another. The filings document the sequence; what legal significance it carries — including whether charitable assets were improperly used to support political-campaign activity — is for the IRS to resolve.

Sources: New Venture Fund, Hopewell Fund, and Windward Fund Forms 990, Schedule I; Sixteen Thirty Fund and North Fund Forms 990, Schedule C; Your Community PAC FEC filings, committee C00886614.

The Network

Four of the five funds use Suite 300 at 1828 L Street NW with different suite-letter suffixes; New Venture Fund reports the same street address in recent years. Every one of them lists its books as kept “in care of” the same company, the for-profit consulting firm Arabella Advisors LLC. In tax year 2024, every one of the five returns was prepared by Baker Tilly Advisory Group LP.

Three are organized as 501(c)(3) public charities, whose donors receive tax deductions and which are barred from intervening in political campaigns: New Venture Fund, Hopewell Fund, and Windward Fund. Two are organized as 501(c)(4) social-welfare organizations, which may engage in political activity and whose donors receive no deduction: Sixteen Thirty Fund and North Fund.

In tax year 2024 alone, the five funds reported combined revenue of $1,505,905,241. New Venture Fund, the largest, reported $662 million in revenue and 732 employees. At the other end sits North Fund: $45 million in revenue, zero employees — and, as a later section shows, $18.4 million in political-campaign spending that year, carried out by an organization with no staff of its own.

Sources: New Venture Fund, Sixteen Thirty Fund, North Fund, Hopewell Fund, and Windward Fund Forms 990 (TY2024), Part I and header.

The Money Flow

Charities and political organizations are different things under federal law, and the line between them is the deductibility of the money and the permissibility of the spending. The Arabella network’s charitable funds moved $389,148,524 across that organizational boundary into its 501(c)(4) funds between 2016 and 2024. The dominant channel runs from New Venture Fund — the largest charity — to Sixteen Thirty Fund, the principal political arm: $315,922,236 over the period, documented on New Venture Fund’s own Schedule I grant disclosures.

The timing tracks the political calendar. In 2020, a presidential year, New Venture Fund sent $86,234,295 to Sixteen Thirty Fund — its largest single-year transfer. That same year, Sixteen Thirty Fund reported $167,053,525 in political-campaign expenditures on its Schedule C. And that same year, Sixteen Thirty Fund reported having zero employees while spending $167 million on political activity.

| Tax Year | New Venture Fund 501(c)(3) → Sixteen Thirty Fund 501(c)(4) |

|---|---|

| 2016 | $1,230,790 |

| 2017 | $20,121,213 |

| 2018 | $26,747,561 |

| 2019 | $33,013,025 |

| 2020 | $86,234,295 |

| 2021 | $27,270,554 |

| 2022 | $34,770,000 |

| 2023 | $27,601,875 |

| 2024 | $58,932,923 |

| Total | $315,922,236 |

The two other charities fed the same political arm: Hopewell Fund and Windward Fund together sent another $28,044,960 to Sixteen Thirty Fund, and the network’s charities sent $45,181,328 to North Fund.

Consolidated, the full charitable-to-political flow across the network — each charity to each political arm, 2016 through 2024 — foots as follows:

| Charity (501(c)(3)) | → Sixteen Thirty Fund (501(c)(4)) | → North Fund (501(c)(4)) | Total to Political Arms |

|---|---|---|---|

| New Venture Fund | $315,922,236 | $44,950,113 | $360,872,349 |

| Hopewell Fund | $25,544,960 | $45,000 | $25,589,960 |

| Windward Fund | $2,500,000 | $186,215 | $2,686,215 |

| Total | $343,967,196 | $45,181,328 | $389,148,524 |

Sources: New Venture Fund Forms 990, Schedule I, Part II, TY2016–TY2024; Hopewell Fund and Windward Fund Forms 990, Schedule I; Sixteen Thirty Fund Form 990, Schedule C (TY2020).

What the Political Arms Did With the Money

Across fifteen entity-years — a complete inventory of every Sixteen Thirty Fund and North Fund return for tax years 2016 through 2024, each figure verified from the funds’ own filings — the two 501(c)(4) funds reported $453,729,094 in political-campaign expenditures on Schedule C.

A large share of those §527 transfers is not itemized by recipient on the face of Schedule C. On Schedule C, a 501(c)(4) reports both the total it routed to political “527” organizations and an itemized list of who received it. Across these fifteen entity-years, the funds reported $420,175,979 in such transfers but itemized only $125,162,564 of it by recipient — leaving $295,013,415 unattributed on the face of the schedules. In tax year 2020 alone, $110,559,183 of Sixteen Thirty Fund’s reported political transfers went unitemized — in the same year the fund reported zero employees and $167 million in political spending.

Sources: Sixteen Thirty Fund and North Fund Forms 990, Schedule C, Part I-A, fifteen entity-years (TY2016–TY2024).

The Trace That Completes Itself

For one downstream recipient, the sequence runs from the charitable network to named federal candidates — each link documented on the parties’ own filings.

Through March 31, 2026, Sixteen Thirty Fund and North Fund — the network’s two 501(c)(4) political funds — together contributed $13,739,642 to a federal super PAC called Your Community PAC (Federal Election Commission committee C00886614). That was about 58.6 percent of the committee’s non-memo itemized receipts reviewed ($13,739,642 of $23,449,005). The two political arms of a network fed by charitable dollars were, by a wide margin, this super PAC’s largest funder.

What the super PAC did with the money is a matter of public record at the FEC. Your Community PAC reported $19,799,415 in independent expenditures naming federal candidates — $12,718,076 of it supporting the 2024 Democratic presidential nominee, Kamala Harris. The rest backed or attacked candidates in contested 2024 House and Senate races: ten federal candidates in all, four Democrats and one independent supported, and five Republicans opposed.

| Candidate | Office / Party | Support / Oppose | Independent Expenditures |

|---|---|---|---|

| Kamala Harris | President / Dem | Support | $12,718,076 |

| Jon Tester | Senate / Dem | Support | $1,829,235 |

| Carl Marlinga | House / Dem | Support | $1,399,994 |

| Monica Tranel | House / Dem | Support | $427,361 |

| Jonathan Thorp | House / Ind | Support | $28,157 |

| Derrick Van Orden | House / Rep | Oppose | $957,765 |

| Zach Nunn | House / Rep | Oppose | $908,429 |

| Matthew Van Epps | House / Rep | Oppose | $738,001 |

| Bernie Moreno | Senate / Rep | Oppose | $601,833 |

| Don Bacon | House / Rep | Oppose | $190,563 |

The $19.9 million total includes 2024 expenditures and a smaller 2025 Tennessee House-race component reported in the raw FEC Schedule E data.

One precision the record requires: money is fungible, and Your Community PAC also took in funds from other donors, so no claim is made that a specific charitable dollar bought a specific advertisement. What the filings establish is narrower and harder to wave away — the Arabella network’s two political funds were this committee’s majority funder during the very period it spent $19.9 million naming federal candidates, and each step along the path from charitable-network funding to candidate-related expenditure appears on the parties’ own filings.

Sources: Your Community PAC FEC filings, committee C00886614 — Schedule A receipts and Schedule E independent expenditures; Sixteen Thirty Fund and North Fund Forms 990, Schedule I / Schedule C (TY2024).

What the Returns Don’t Say

Here is the part that the filings themselves make difficult to explain.

Federal Form 990 includes Schedule R, where an organization discloses its related organizations. Across twenty-seven entity-years, the four sibling funds filed no Schedule R at all — each answering “no” to the questions that would require it. New Venture Fund did file Schedule R every year, but listed only its own subsidiaries; in no year did it name Sixteen Thirty Fund, North Fund, Hopewell Fund, or Windward Fund. Five funds sharing one manager, overlapping addresses, one accounting firm in tax year 2024, recurring cross-grants, and — for Sixteen Thirty Fund and North Fund — a New Venture Fund payroll-agent arrangement, disclose on their tax returns no relationship to one another.

The returns also changed in a way that coincides with a change in the network’s public ownership. Through tax year 2020, four of the funds filed Schedule L — the schedule for transactions with “interested persons” — disclosing that Arabella Advisors was a “35% controlled entity” of Eric Kessler, then serving in a board role within the network. Beginning in tax year 2021, those Schedule L disclosures stopped at those four funds and did not resume through 2024 — even as payments to Arabella continued at $21 million to $33 million a year from New Venture Fund alone. Across the period, the network’s funds paid Arabella Advisors approximately $312 million.

And on this point, the funds’ own audited financial statements and their tax returns appear to take different reporting positions: the audits treat the Arabella relationship as a related-party matter requiring director recusal, while the Forms 990 disclose Arabella as a contractor but answer “no” to the business-transaction questions that would trigger Schedule L reporting. The 2024 audited financial statements of Sixteen Thirty Fund and Windward Fund each state that “a board director of the Fund has a direct financial interest in Arabella,” describe the director’s recusal from votes involving the firm, and treat the arrangement as a related-party transaction. The same funds’ 2024 Form 990 returns answer “no” to the business-transaction questions that would trigger Schedule L, and file none.

Why the Schedule L disclosures stopped when they did is not a mystery the public record resolves. Eric Kessler has said publicly, and the Chronicle of Philanthropy has reported, that he sold majority ownership of Arabella in 2020. If that sale reduced his combined interest below the 35-percent threshold, the cessation would follow from the instructions rather than from any concealment. What the public record does not show — and what only the relevant authorities can determine from ownership records not available publicly — is what percentage Kessler and his co-owner Bruce Boyd held after the sale, and whether related-party interests are counted toward that threshold. The question is narrow and factual. The answer is in records that are not public.

The payments to Arabella continued regardless. New Venture Fund alone paid Arabella Advisors $214,233,341 across the nine years examined — an average of roughly $24 million a year — to a firm whose owner was disclosed on New Venture’s own returns as board chair in 2016 and 2017, secretary in 2018 and 2019, and former board secretary in 2020. Across all five funds, the total paid to Arabella Advisors and affiliated Arabella-branded management entities across the period reaches approximately $312 million. The returns report the payments in Part VII contractor disclosures and Schedule O narratives. They do not report them on Schedule L after tax year 2020.

One subsequent development bears noting. In November 2025 — after the tax years covered by this article — Arabella Advisors announced its dissolution. Its administrative-services business was acquired by a new entity called Sunflower Services, described by New Venture Fund’s president as owned by the nonprofits themselves. The period after tax year 2024 is outside the verified record here. But the dissolution is relevant to anyone examining these patterns: it raises questions about document preservation, about whether the management relationship continues under a new name and structure, and about what the ownership records from the Arabella years will show if examined.

Sources: New Venture Fund, Sixteen Thirty Fund, North Fund, Hopewell Fund, and Windward Fund Forms 990, Schedule R and Schedule L; Sixteen Thirty Fund and Windward Fund audited financial statements (TY2024), related-party notes; New Venture Fund Form 990, Part VII contractor disclosures; Chronicle of Philanthropy reporting on the 2020 Arabella sale.

The Charity That Staffs the Political Fund

North Fund — a 501(c)(4) — spent $18,405,128 on political-campaign activity in 2024 with zero employees of its own. Its return, and Sixteen Thirty Fund’s, disclose how the work gets done: New Venture Fund — a 501(c)(3) charity, and described in the disclosure as “an unaffiliated organization” — serves as their payroll agent. A charity supplies the workforce through which a political fund with no employees of its own spends millions on political activity.

Sources: North Fund and Sixteen Thirty Fund Forms 990, Schedule O (common-paymaster disclosure) and Schedule C (TY2024).

What This Is

The Arabella network is separate from, and independent of, the Soros/Tides network documented in prior reporting at this site; it stands on its own evidentiary record. That record is not a set of leaked memos or anonymous sources. It is the funds’ own federal tax returns, their own audited financial statements, and the FEC filings of the committee they funded.

What those documents describe is a structure in which tax-deductible and social-welfare dollars enter a network of commonly managed funds, are reported by the receiving funds as political transfers, are routed to a federal super PAC during a campaign, and are spent on independent expenditures naming federal candidates — while the funds disclose, on the returns where disclosure is required, no relationship to one another.

The defense of such an arrangement is always its form: separate boards, separate EINs, arm’s-length contracts, and a manager that is technically a vendor rather than a parent. But federal tax law does not stop at the form. It asks what the arrangement is in substance — and the substance here is five funds that share overlapping addresses, a manager, a common 2024 return preparer, and, for the two 501(c)(4) arms, a charity-based payroll arrangement, while moving money along a documented sequence and reporting no related-organization relationship among them. Whether the form survives that scrutiny is not a question this article answers. It is the question the documents raise.

I have filed a whistleblower complaint with the Internal Revenue Service documenting these patterns, with the underlying figures traced to primary-source filings. The IRS is the body that decides what the law makes of the conduct; this article makes no such finding. It reports what the documents say.

Sources: as cited in the sections above — the five funds’ Forms 990, their audited financial statements, and Your Community PAC’s FEC filings.

Public Record Disclaimer: All findings in this article are based on publicly available records, including IRS Form 990 filings, audited financial statements prepared by independent accounting firms and obtained from the New York State Attorney General’s public Charities Registry, and Federal Election Commission disclosures. This analysis reflects a good-faith review of documentary evidence on matters of public concern.

Written by Sam Antar | Forensic Accountant.

For updates on this investigation, follow @SamAntar on X.

© 2026 Sam E. Antar. All rights reserved.